Individual clinician entrepreneurs have the deck stacked against them. Admin and compliance work sucks time, and the risk of errors is high. Given their size, they have limited negotiation power to get higher insurance reimbursement rates. A fantastic clinician is not necessarily a great marketer.

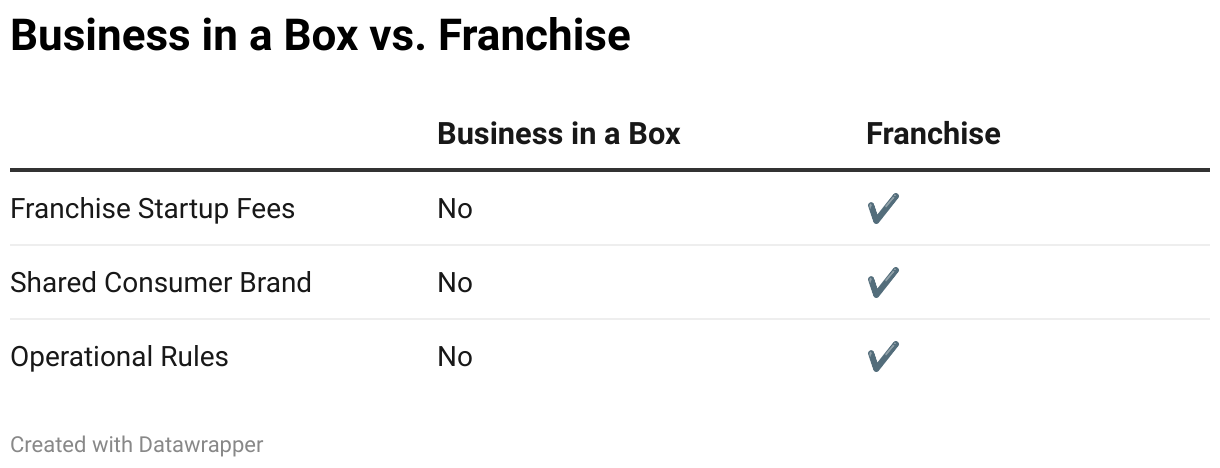

A new model, the healthcare "business in a box," has emerged that helps with all of these impediments without the tighter constraints of a franchise or employment. It provides clinicians with a solution to start their own practices, simplifying the process of becoming healthcare entrepreneurs by offering a complete package for establishing a private practice.

To understand adoption of this model, we developed a dataset of all clinicians affiliated with all identified “business in a box” platforms. We did this by using data from web crawlers that index all of the pages on these platform websites, as well as inbound links to their websites. In total we analyzed 77,100 clinician profiles across the platforms.

This analysis enabled us to identify the platforms experiencing the most rapid growth, assess their scale, and pinpoint the specialties with the highest adoption rates. See Methodology section for more details.

For the sake of this analysis, we define a healthcare "business in a box" platform by the following characteristics:

While similar models exist, such as franchises and Management Services Organizations (MSOs) (see footnote on MSO vs. BIAB), our focus remains on platforms that closely align with this specific definition.

There has been a significant rise in “business in a box” platforms in recent years. This growth is likely fueled by several factors, including clinician burnout in traditional healthcare settings, the expansion of clinicians’ scope of practice, and the increasing number of Advanced Practice Clinicians (APCs) and Licensed Professional Counselors (LPCs).

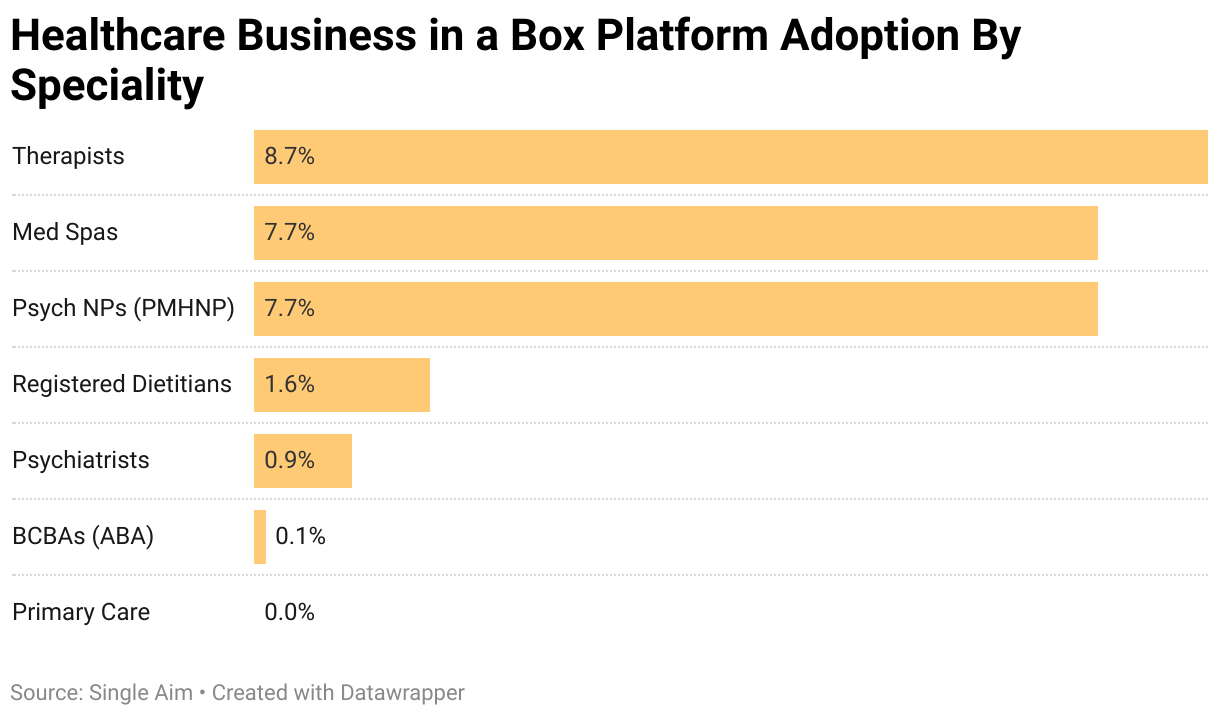

Therapists, Psychiatric Nurse Practitioners, and RN owners of med spas have led the way in adoption of "business in a box" platforms.

We will go one-by-one through the specialties and explore the data to understand what makes a “business in a box” platform successful. These adoption rates are our best estimates and depend on the accuracy of the chosen numerator and denominator. See Methodology for more information.

Med spas are a rapidly growing segment of the healthcare industry, with around 8,800 locations in the US. Franchising has long been a popular model for med spa ownership. Recently, there has been a surge in “business in a box” platforms targeting this industry. The med spa business is a good fit for a "business in a box" platform for the following reasons:

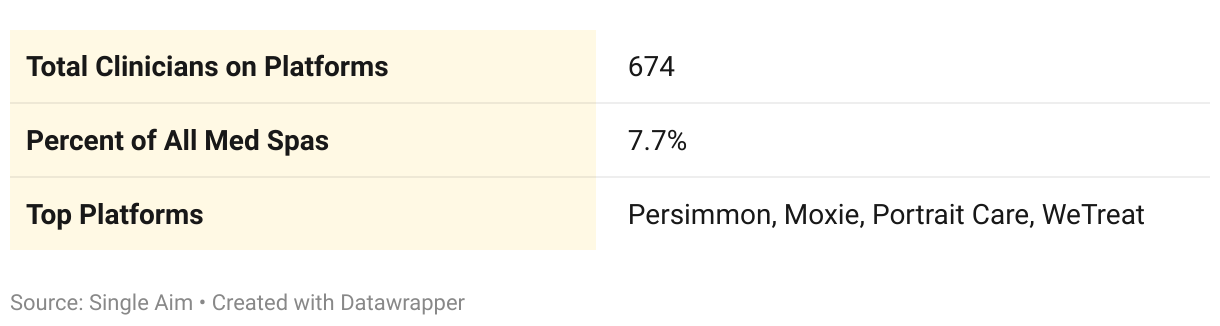

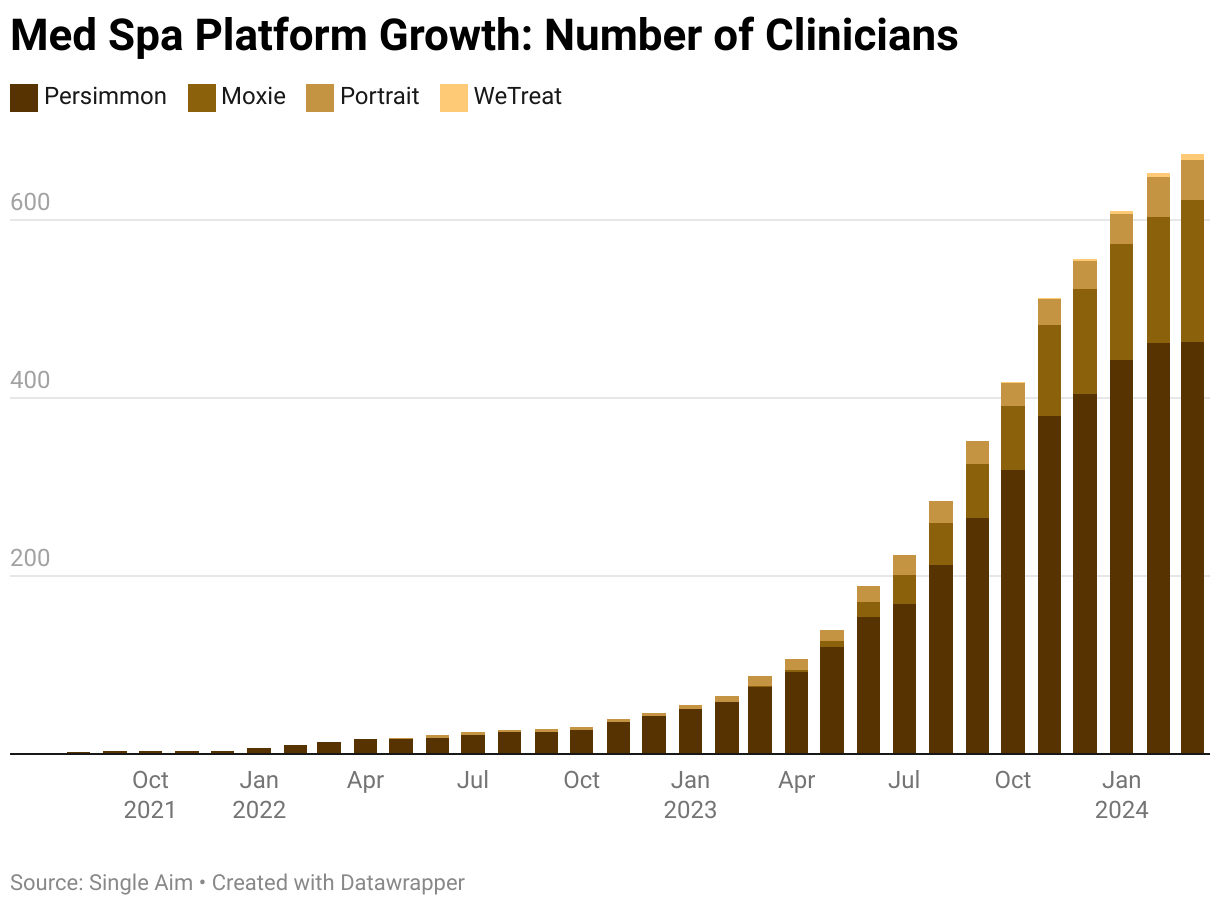

The top platforms are Persimmon, Moxie, Portrait Care and WeTreat. Med spas can offer many different services (sometimes involving expensive medical devices). The med spa “business in a box” platforms generally prepare clinicians for lighter weight businesses focused on injectables such as botox and fillers.

These platforms offer comprehensive solutions for prospective med spa owners, including:

These platforms typically charge fees of 8-9% of gross revenue. Given that med spa profit margins typically range from 20-25%, this translates to 36-40% of profits being directed to the platform.

While experiencing rapid growth, “business in a box” platforms still represent a small portion of the overall med spa market. We estimate 7.7% (674 out of 8,800) of med spas in the US operate under this model.

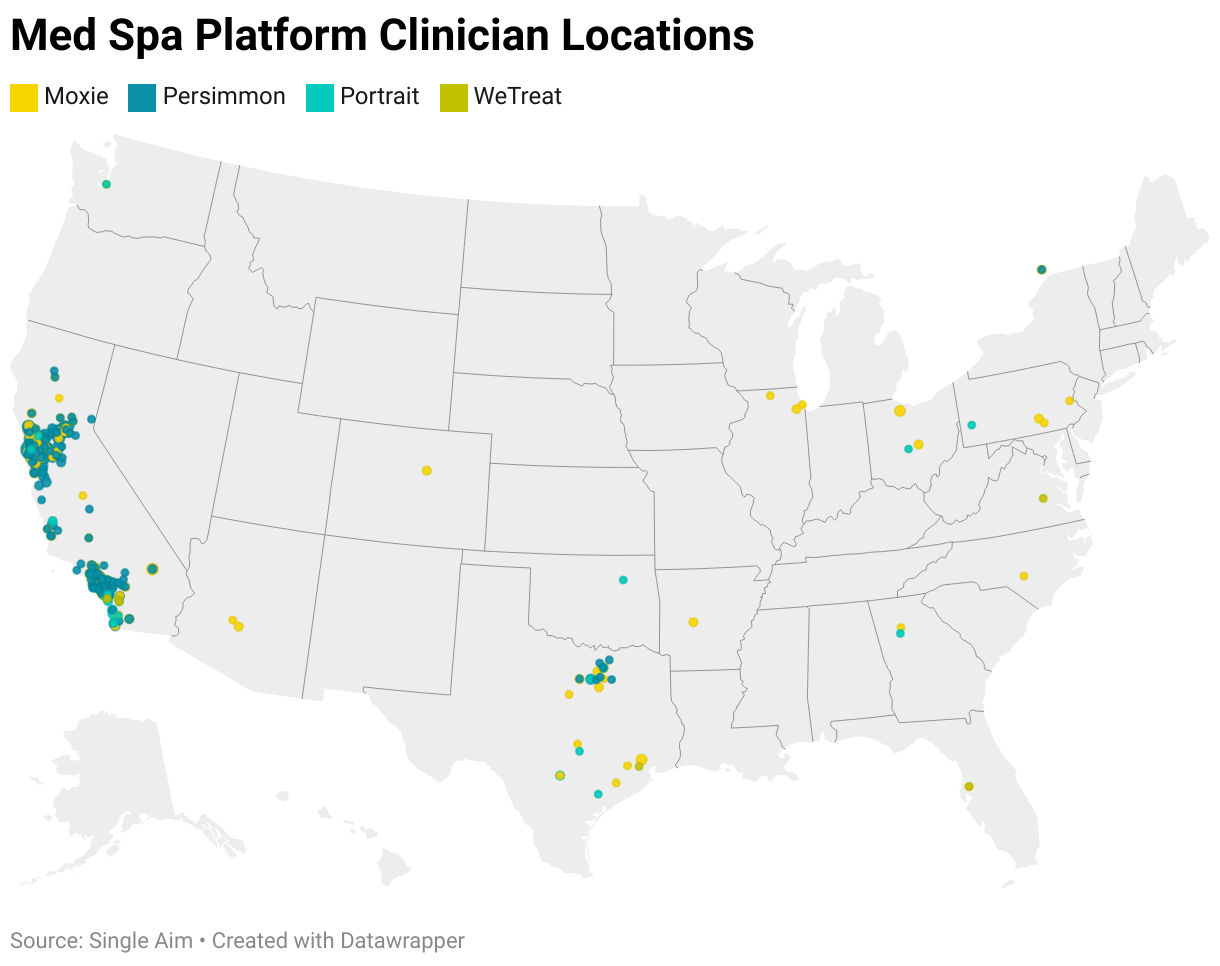

Interestingly, our data shows, the med spa businesses started on these platforms are highly concentrated in California and Texas.

Comparatively around 25% of US based med spas are based in California or Texas. This indicates there is a long growth pathway for these platforms (or new entrants) to serve the entire United States.

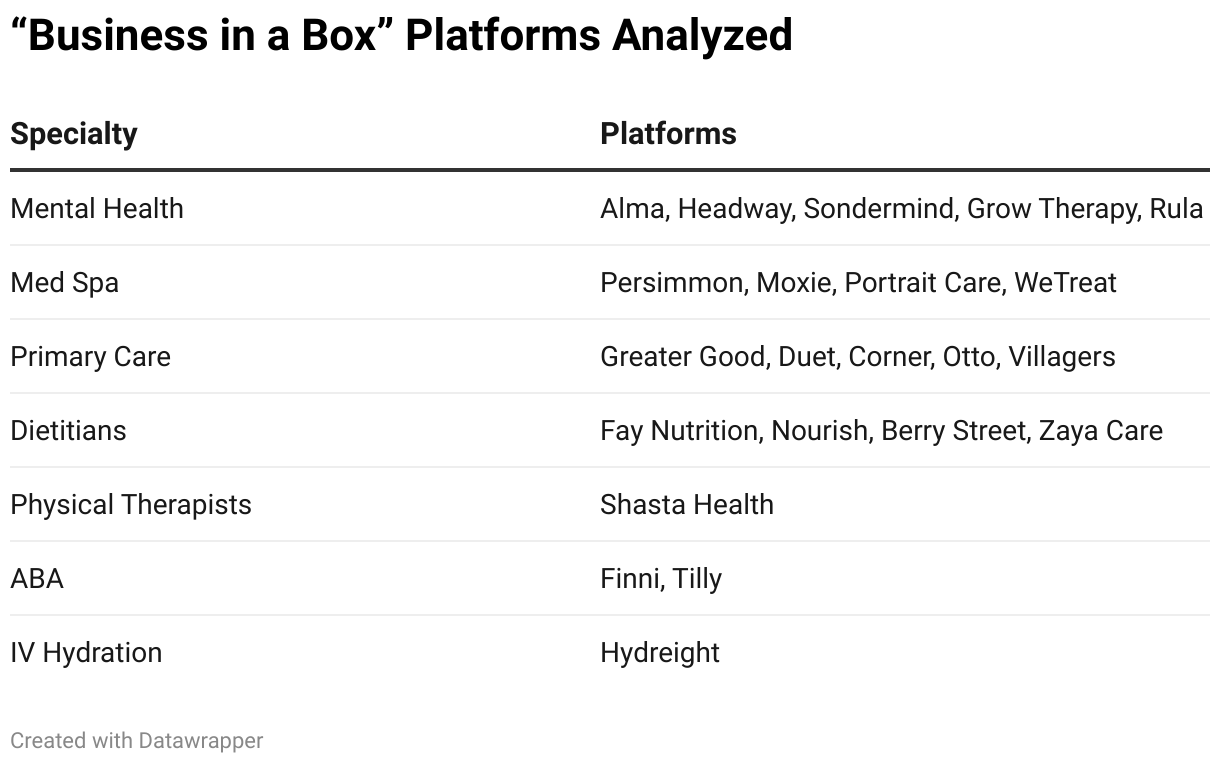

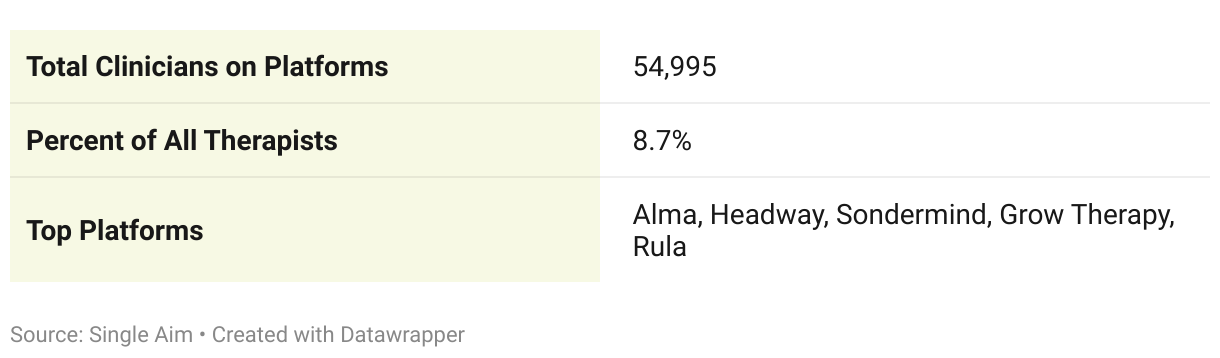

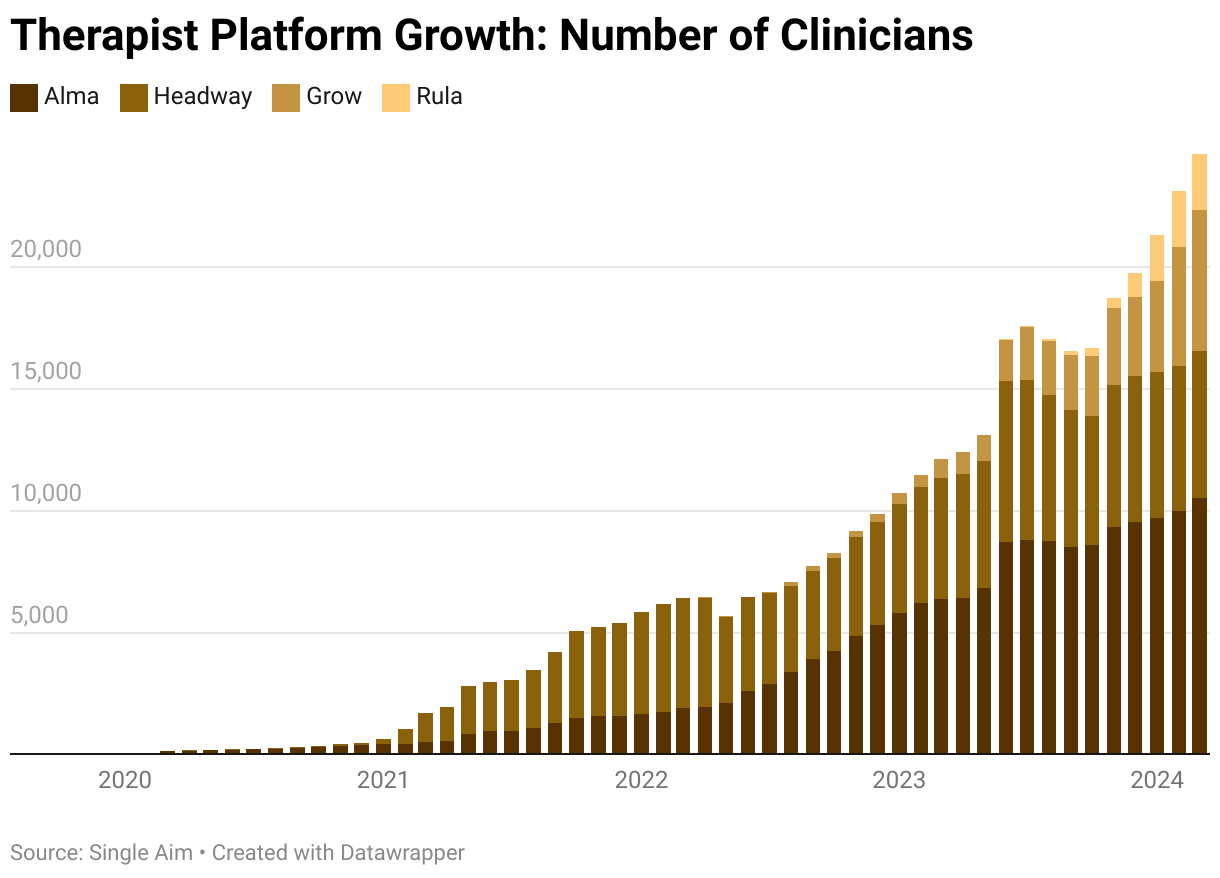

"Business in a box" platforms have achieved their greatest scale within the therapy sector. We estimate 8.7% of all practicing therapists in the US, approximately 55,000 clinicians, utilize these platforms for their businesses.

Several factors make therapy highly compatible with this model:

In return, therapists often give up 20-30% of billed revenue to the platform. Because these "business in a box" platforms don't provide comprehensive business support, many therapists seek complementary services such as accounting from external companies.

Adoption rates of these platforms vary significantly among therapy specialties. Our data shows Licensed Professional Counselors (LPCs) have the highest adoption at around 10%, followed by Licensed Clinical Social Workers (LCSWs) and Licensed Marriage and Family Therapists (LMFTs) at roughly 3%. Adoption among psychologists remains very low at 0.2%.

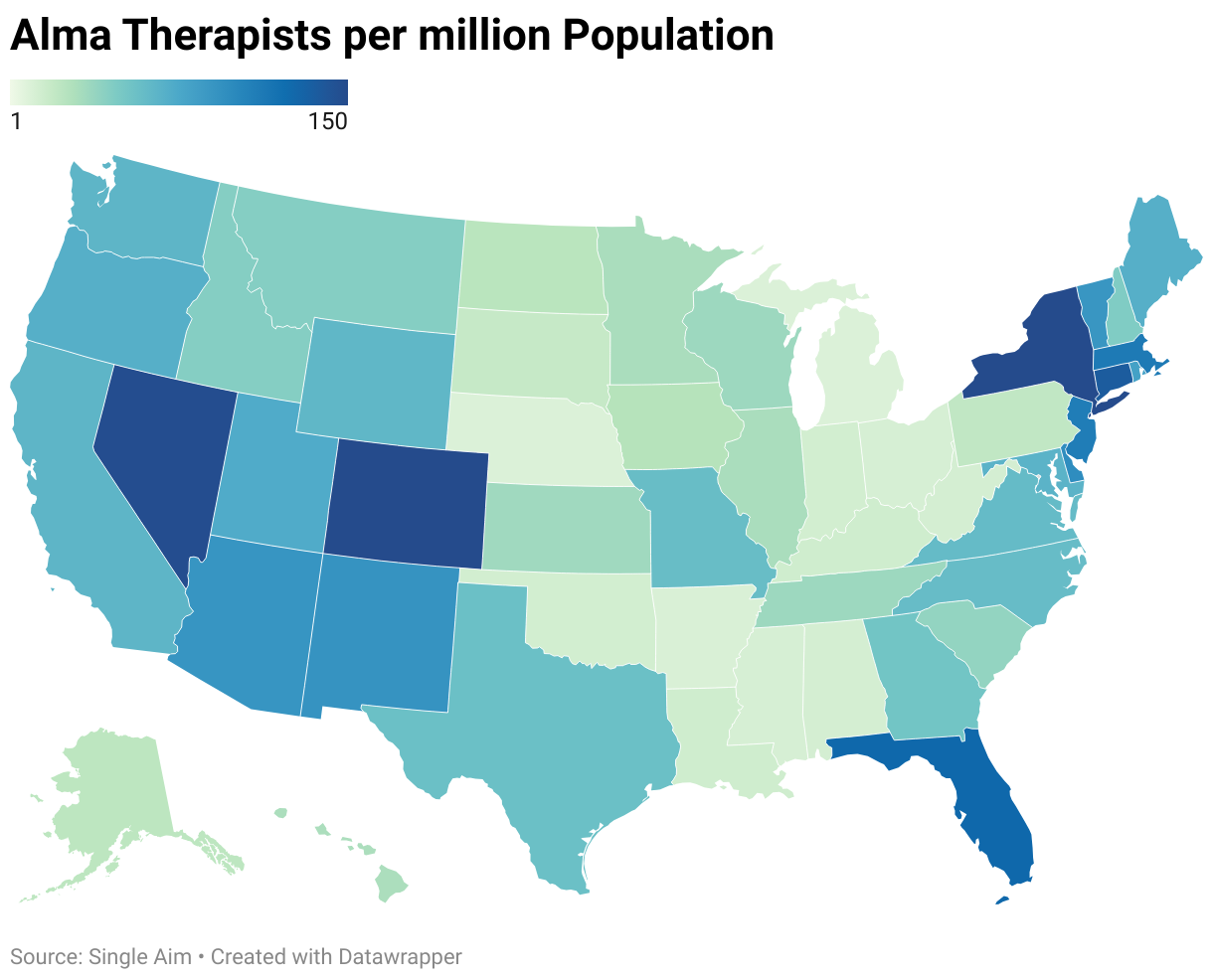

Unlike med spa, therapy platforms have widespread nationwide scale. Since therapy can be provided remotely and therapists can get licenses in many states, it is easier for these platforms to serve the entire nation. Regardless, there still exist significant geographic disparities. For example, our data shows Alma has 150 licensed therapists per million people in New York state while having only 11 per million in Michigan.

We expect the therapy platforms to continue to grow through further geographic density and into new health plan coverage. These platforms have focused almost exclusively on commercially insured patients. Conversations with therapists on the platforms reveal that many are getting their own Medicaid and Medicare contracts, given huge unmet demand for patients with these payers and competition among therapists for commercially insured patients. Securing these contracts is likely to be the next growth avenue, further mainstreaming these platforms.

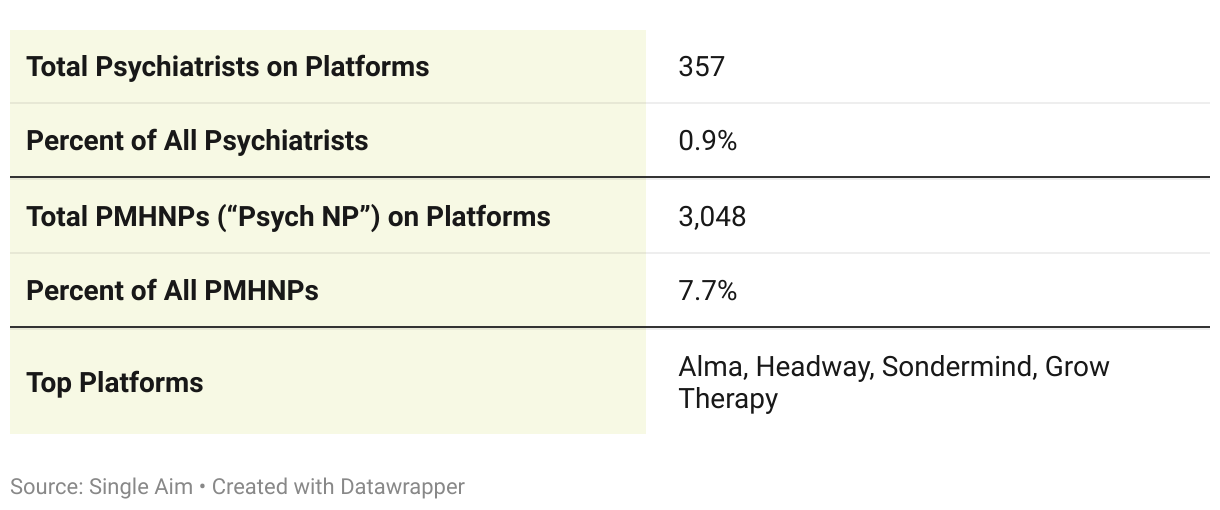

The "business in a box" platforms that have attracted therapists have also seen similar adoption (7.7%) among Psychiatric Mental Health Nurse Practitioners (PMHNPs). However, psychiatrist adoption is significantly lower at just 0.9%. This disparity could be due to several factors:

We expect adoption to continue growing among Psych NPs, especially if the platforms move into serving Medicaid and Medicare patients. It is unclear to us if adoption will increase among psychiatrists since it is currently so comparatively low.

Unlike within mental health and med spas, we did not identify any scaled "business in a box" platforms designed specifically for primary care. However, adjacent models and organizations do provide some relevant insights:

The absence of large-scale primary care platforms on the "business in a box" model likely stems from several factors:

New payment models emphasizing value-based care could potentially make primary care a more attractive niche for "business in a box" platforms in the future. In fact, this is the approach the emerging primary care platforms are using.

Our analysis has shown the healthcare "business in a box" platforms have emerged and grown quickly in the last 5 years. Most of this growth has occurred in specialities that see the most organic clinical entrepreneurial activity, mental health and aesthetics. The scaled "business in a box" platforms such as Alma or Moxie have proven the need for the model and we expect it to only continue growing. Continued growth will primarily follow three pathways. First, further adoption in existing verticals through geographic and payer expansion. Second, growth of nascent specialities such as primary care and physical therapy likely through payment model innovation. Lastly, many more niche platforms will emerge in specialities with existing entrepreneurialism such as home care, wound care, ketamine, pediatric therapy, and addiction to name a few. It's a good time to be a clinician entrepreneur.

There are a handful of scaled platforms with registered dietitians. These platforms are very similar to the mental health therapist platforms in terms of features: insurance contracting, insurance billing, EHR, and some demand generation. Across Fay Nutrition, Nourish, Berry Street, and Zaya Care, we counted 1752 clinicians on our data set, presenting an adoption of these platforms among registered dietitians at 1.6%

Some of these platforms have closer employment relationships with their nutritionists. For example, Nourish hires its nutritionists as employees. This shows the gray area between “business in a box” platforms and traditional employment.

There are many options available for physical therapists outside of traditional employment. There are many franchise businesses such as FYZICAL with 535 locations. There are also contractor or “gig” platforms like Luna Physical Therapy with “thousands of physical therapists”.

We are aware of only one “business in a box” platform for physical therapists, Shasta Health, but in our data set only appears to have 3 clinicians. This is likely an area to see significant growth given the existing prominence of franchises and contractor platforms.

The IV hydration sector has witnessed explosive growth since the mid-2010s, with thousands of clinics now operating across the US. Businesses in this space adopt both franchise and "business in a box" models.

Dripbar, a prominent franchise with 96 locations, provides a well-established model for IV hydration businesses. Hydreight, representing the "business in a box" approach, boasts a network of 104 locations. This is a vertical well fit for a “business in a box” platform since the investment required is low and the clinician owners are mostly RNs.

Applied Behavior Analysis (ABA), a therapy for children with autism, has experienced significant growth and industry consolidation over the past two decades. While most clinicians (BCBAs and RBTs) work within larger practices, emerging "business in a box" platforms empower clinicians to establish their own businesses.

Finni Health and Tilly Therapy are two such platforms, Finni supports 39 BCBAs in running their own practices, and Tilly supports 25 BCBAs. However, with approximately 66,000 total BCBAs in the US, the current adoption rate of "business in a box" solutions in ABA remains low at only 0.1%. Running an ABA practice is more operationally complex than a med spa or therapy practice since in most cases the BCBA needs to manage a team of RBTs. This likely selects out clinicians who don’t want to recruit and manage a team which could explain the lower adoption rates.

There are many franchise organizations to start a lab testing company. For example, ARCPoint Labs has 157 locations. We are unaware of any “business in a box” platforms for labs.

The home health sector offers ample opportunities for franchising, as evidenced by the approximately 350 locations of Nurse Next Door. However, we couldn't identify any scaled "business in a box" platforms specifically designed for home health businesses. This absence suggests a potential opportunity for the emergence of such platforms in the near future, offering clinicians and entrepreneurs a new model for establishing home health services.

To develop the data in this report, we collected data from web crawlers that index all the pages of websites and all of the links between websites. We were able to identify provider counts for each platform by analyzing all of the “Provider Pages” on the platform. For example, here is a list of all providers on Headway. Some platforms don’t have Provider Pages and instead provide tools which their providers link to from their websites. For example Moxie med spas link to “app.joinmoxie.com/”. In these cases, we totaled external websites linking to platforms through these links.

The provider counts for platforms are limited by the completeness of the web crawlers indexing of available pages and links. We don’t expect this to catch 100% of pages. Take the numbers in this report as directional.

We expected some clinicians to use multiple platforms. In a quick analysis of therapy platforms, we saw 20% of profiles were duplicated across platforms. So, in our analyses we reduced the number of estimated clinicians by 20%.

To develop a percent adoption rate, we needed to know the total number of clinicians and clinics of certain specialties in the United States. We found getting reliable estimates of this was difficult. We will share the sources we used.

Fair Use: Feel free to use this data and research with proper attribution linking to this study.

Media Inquiries: For media inquiries, contact team@singleaimhealth.com

Thanks to Danielle Clanaman, Kusum Chanrai, Maxine Whitely, Meghan Jewitt, Alex Bargar, Heather Wake, Mary Tindall, Sonny Mo, and others for reviewing this article.

Management Service Organizations or MSOs have many versions in the healthcare industry. Actually, most “business in a box platforms” are MSOs since they need to be in order to operation within corporate practice of medicine regulations. There is a certain type of MSO that partners with existing clinician businesses to support their operations. Some examples would be Aledade or Privia in primary care. We differentiate this type of MSO from a “business in a box” in that a “business in a box” is focused on forming new businesses, while the MSO is mostly focused on supporting the operations of existing businesses.

Individual clinician entrepreneurs have the deck stacked against them. Admin and compliance work sucks time, and the risk of errors is high. Given their size, they have limited negotiation power to get higher insurance reimbursement rates. A fantastic clinician is not necessarily a great marketer.

A new model, the healthcare "business in a box," has emerged that helps with all of these impediments without the tighter constraints of a franchise or employment. It provides clinicians with a solution to start their own practices, simplifying the process of becoming healthcare entrepreneurs by offering a complete package for establishing a private practice.

To understand adoption of this model, we developed a dataset of all clinicians affiliated with all identified “business in a box” platforms. We did this by using data from web crawlers that index all of the pages on these platform websites, as well as inbound links to their websites. In total we analyzed 77,100 clinician profiles across the platforms.

This analysis enabled us to identify the platforms experiencing the most rapid growth, assess their scale, and pinpoint the specialties with the highest adoption rates. See Methodology section for more details.

For the sake of this analysis, we define a healthcare "business in a box" platform by the following characteristics:

While similar models exist, such as franchises and Management Services Organizations (MSOs) (see footnote on MSO vs. BIAB), our focus remains on platforms that closely align with this specific definition.

There has been a significant rise in “business in a box” platforms in recent years. This growth is likely fueled by several factors, including clinician burnout in traditional healthcare settings, the expansion of clinicians’ scope of practice, and the increasing number of Advanced Practice Clinicians (APCs) and Licensed Professional Counselors (LPCs).

Therapists, Psychiatric Nurse Practitioners, and RN owners of med spas have led the way in adoption of "business in a box" platforms.

We will go one-by-one through the specialties and explore the data to understand what makes a “business in a box” platform successful. These adoption rates are our best estimates and depend on the accuracy of the chosen numerator and denominator. See Methodology for more information.

Med spas are a rapidly growing segment of the healthcare industry, with around 8,800 locations in the US. Franchising has long been a popular model for med spa ownership. Recently, there has been a surge in “business in a box” platforms targeting this industry. The med spa business is a good fit for a "business in a box" platform for the following reasons:

The top platforms are Persimmon, Moxie, Portrait Care and WeTreat. Med spas can offer many different services (sometimes involving expensive medical devices). The med spa “business in a box” platforms generally prepare clinicians for lighter weight businesses focused on injectables such as botox and fillers.

These platforms offer comprehensive solutions for prospective med spa owners, including:

These platforms typically charge fees of 8-9% of gross revenue. Given that med spa profit margins typically range from 20-25%, this translates to 36-40% of profits being directed to the platform.

While experiencing rapid growth, “business in a box” platforms still represent a small portion of the overall med spa market. We estimate 7.7% (674 out of 8,800) of med spas in the US operate under this model.

Interestingly, our data shows, the med spa businesses started on these platforms are highly concentrated in California and Texas.

Comparatively around 25% of US based med spas are based in California or Texas. This indicates there is a long growth pathway for these platforms (or new entrants) to serve the entire United States.

"Business in a box" platforms have achieved their greatest scale within the therapy sector. We estimate 8.7% of all practicing therapists in the US, approximately 55,000 clinicians, utilize these platforms for their businesses.

Several factors make therapy highly compatible with this model:

In return, therapists often give up 20-30% of billed revenue to the platform. Because these "business in a box" platforms don't provide comprehensive business support, many therapists seek complementary services such as accounting from external companies.

Adoption rates of these platforms vary significantly among therapy specialties. Our data shows Licensed Professional Counselors (LPCs) have the highest adoption at around 10%, followed by Licensed Clinical Social Workers (LCSWs) and Licensed Marriage and Family Therapists (LMFTs) at roughly 3%. Adoption among psychologists remains very low at 0.2%.

Unlike med spa, therapy platforms have widespread nationwide scale. Since therapy can be provided remotely and therapists can get licenses in many states, it is easier for these platforms to serve the entire nation. Regardless, there still exist significant geographic disparities. For example, our data shows Alma has 150 licensed therapists per million people in New York state while having only 11 per million in Michigan.

We expect the therapy platforms to continue to grow through further geographic density and into new health plan coverage. These platforms have focused almost exclusively on commercially insured patients. Conversations with therapists on the platforms reveal that many are getting their own Medicaid and Medicare contracts, given huge unmet demand for patients with these payers and competition among therapists for commercially insured patients. Securing these contracts is likely to be the next growth avenue, further mainstreaming these platforms.

The "business in a box" platforms that have attracted therapists have also seen similar adoption (7.7%) among Psychiatric Mental Health Nurse Practitioners (PMHNPs). However, psychiatrist adoption is significantly lower at just 0.9%. This disparity could be due to several factors:

We expect adoption to continue growing among Psych NPs, especially if the platforms move into serving Medicaid and Medicare patients. It is unclear to us if adoption will increase among psychiatrists since it is currently so comparatively low.

Unlike within mental health and med spas, we did not identify any scaled "business in a box" platforms designed specifically for primary care. However, adjacent models and organizations do provide some relevant insights:

The absence of large-scale primary care platforms on the "business in a box" model likely stems from several factors:

New payment models emphasizing value-based care could potentially make primary care a more attractive niche for "business in a box" platforms in the future. In fact, this is the approach the emerging primary care platforms are using.

Our analysis has shown the healthcare "business in a box" platforms have emerged and grown quickly in the last 5 years. Most of this growth has occurred in specialities that see the most organic clinical entrepreneurial activity, mental health and aesthetics. The scaled "business in a box" platforms such as Alma or Moxie have proven the need for the model and we expect it to only continue growing. Continued growth will primarily follow three pathways. First, further adoption in existing verticals through geographic and payer expansion. Second, growth of nascent specialities such as primary care and physical therapy likely through payment model innovation. Lastly, many more niche platforms will emerge in specialities with existing entrepreneurialism such as home care, wound care, ketamine, pediatric therapy, and addiction to name a few. It's a good time to be a clinician entrepreneur.

There are a handful of scaled platforms with registered dietitians. These platforms are very similar to the mental health therapist platforms in terms of features: insurance contracting, insurance billing, EHR, and some demand generation. Across Fay Nutrition, Nourish, Berry Street, and Zaya Care, we counted 1752 clinicians on our data set, presenting an adoption of these platforms among registered dietitians at 1.6%

Some of these platforms have closer employment relationships with their nutritionists. For example, Nourish hires its nutritionists as employees. This shows the gray area between “business in a box” platforms and traditional employment.

There are many options available for physical therapists outside of traditional employment. There are many franchise businesses such as FYZICAL with 535 locations. There are also contractor or “gig” platforms like Luna Physical Therapy with “thousands of physical therapists”.

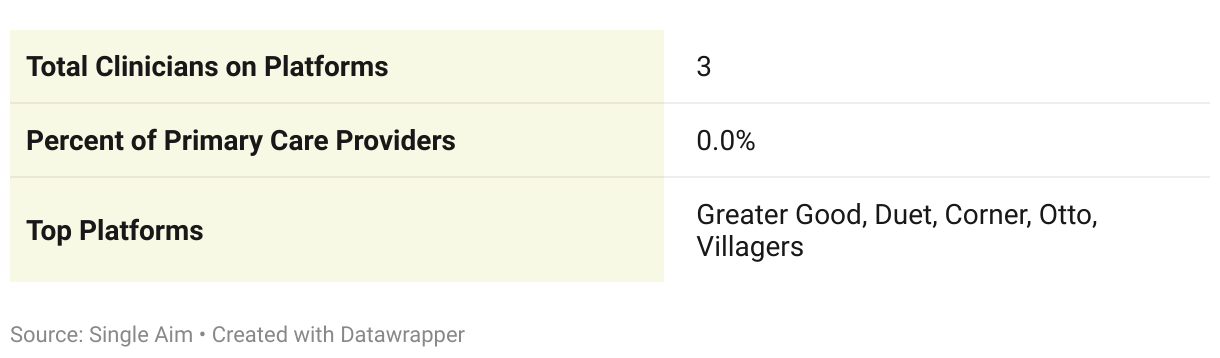

We are aware of only one “business in a box” platform for physical therapists, Shasta Health, but in our data set only appears to have 3 clinicians. This is likely an area to see significant growth given the existing prominence of franchises and contractor platforms.

The IV hydration sector has witnessed explosive growth since the mid-2010s, with thousands of clinics now operating across the US. Businesses in this space adopt both franchise and "business in a box" models.

Dripbar, a prominent franchise with 96 locations, provides a well-established model for IV hydration businesses. Hydreight, representing the "business in a box" approach, boasts a network of 104 locations. This is a vertical well fit for a “business in a box” platform since the investment required is low and the clinician owners are mostly RNs.

Applied Behavior Analysis (ABA), a therapy for children with autism, has experienced significant growth and industry consolidation over the past two decades. While most clinicians (BCBAs and RBTs) work within larger practices, emerging "business in a box" platforms empower clinicians to establish their own businesses.

Finni Health and Tilly Therapy are two such platforms, Finni supports 39 BCBAs in running their own practices, and Tilly supports 25 BCBAs. However, with approximately 66,000 total BCBAs in the US, the current adoption rate of "business in a box" solutions in ABA remains low at only 0.1%. Running an ABA practice is more operationally complex than a med spa or therapy practice since in most cases the BCBA needs to manage a team of RBTs. This likely selects out clinicians who don’t want to recruit and manage a team which could explain the lower adoption rates.

There are many franchise organizations to start a lab testing company. For example, ARCPoint Labs has 157 locations. We are unaware of any “business in a box” platforms for labs.

The home health sector offers ample opportunities for franchising, as evidenced by the approximately 350 locations of Nurse Next Door. However, we couldn't identify any scaled "business in a box" platforms specifically designed for home health businesses. This absence suggests a potential opportunity for the emergence of such platforms in the near future, offering clinicians and entrepreneurs a new model for establishing home health services.

To develop the data in this report, we collected data from web crawlers that index all the pages of websites and all of the links between websites. We were able to identify provider counts for each platform by analyzing all of the “Provider Pages” on the platform. For example, here is a list of all providers on Headway. Some platforms don’t have Provider Pages and instead provide tools which their providers link to from their websites. For example Moxie med spas link to “app.joinmoxie.com/”. In these cases, we totaled external websites linking to platforms through these links.

The provider counts for platforms are limited by the completeness of the web crawlers indexing of available pages and links. We don’t expect this to catch 100% of pages. Take the numbers in this report as directional.

We expected some clinicians to use multiple platforms. In a quick analysis of therapy platforms, we saw 20% of profiles were duplicated across platforms. So, in our analyses we reduced the number of estimated clinicians by 20%.

To develop a percent adoption rate, we needed to know the total number of clinicians and clinics of certain specialties in the United States. We found getting reliable estimates of this was difficult. We will share the sources we used.

Fair Use: Feel free to use this data and research with proper attribution linking to this study.

Media Inquiries: For media inquiries, contact team@singleaimhealth.com

Thanks to Danielle Clanaman, Kusum Chanrai, Maxine Whitely, Meghan Jewitt, Alex Bargar, Heather Wake, Mary Tindall, Sonny Mo, and others for reviewing this article.

Management Service Organizations or MSOs have many versions in the healthcare industry. Actually, most “business in a box platforms” are MSOs since they need to be in order to operation within corporate practice of medicine regulations. There is a certain type of MSO that partners with existing clinician businesses to support their operations. Some examples would be Aledade or Privia in primary care. We differentiate this type of MSO from a “business in a box” in that a “business in a box” is focused on forming new businesses, while the MSO is mostly focused on supporting the operations of existing businesses.

Chris, founded Single Aim Health in 2024 to provide clinicians, especially NPs and PAs, with essential services for launching and growing their practices. A Stanford graduate in Product Design, Chris co-founded Momentus Media, which was acquired by Facebook, and worked as a Product Manager there. He later gained expertise in digital health through leadership roles at Bicycle Health, Virta Health, and founding Wink Health. Now, he is using his experience to help clinicians through Single Aim Health.